Ever looked at your bank account and thought… where the heck did all my money go?

🙋♀️ Same.

That’s exactly why I started giving myself a set of simple rules before spending.

These 5 questions have saved me from countless impulse buys and that awful ‘what did I even buy?’ feeling.

I first wrote this list years ago, but I still use it today whenever I feel like cash is flying out of my account faster than I can earn it.

Here’s the thing: every dollar you don’t spend on stuff you don’t need is a dollar that can go toward something you actually care about—whether that’s paying down debt, taking a family holiday, or finally building that emergency fund.

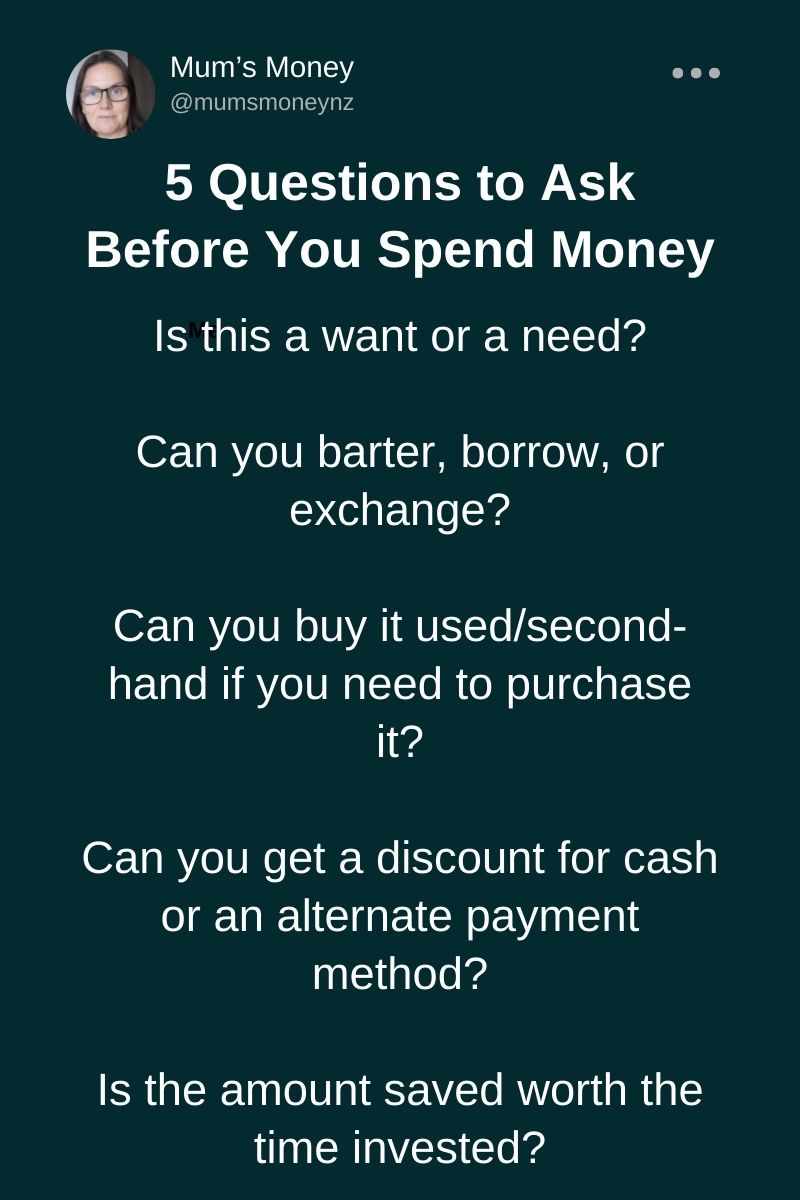

5 Questions I Ask Myself Before Making a Purchase

1. Is this a want or a need?

Depending on where you’re at in your financial journey, some wants might be ok.

Flying home for us was most definitely a need.

Getting new jeans because I’m sick of the same old pair – that’s a want for me.

💡 If it’s not essential, it can probably wait.

2. Can you barter, borrow or exchange?

Does a friend have the item you want?

Could you swap it for something you have?

It doesn’t work for flights, but it could work for a skillsaw you need for a one-off project.

💡 Use your network before you use your wallet.

3. Can you buy it used/second-hand?

If you need it, chances are someone else did at one point.

And they might not need it anymore.

Let them wear the depreciation and buy quality second-hand.

You’ll almost always get a better product if you buy a reputable brand used rather than buying the cheapest brand new.

👉 Example: A second-hand Dyson vacuum on Marketplace might cost the same as a brand-new cheapie that dies in six months. Buy quality, used, and you’ll win every time.

💡 Let someone else pay full price so you don’t have to.

4. Can you get a discount for cash or an alternate payment method?

You won’t know unless you ask.

This could be a cashback offer through a bank or cashback company, an offer through a loyalty program, etc.

You could also search for a coupon code online.

Do your research before you part with those hard-earned dollars.

💡 There’s almost always a discount hiding somewhere—ask, click, or Google before you buy.

5. Is the amount saved worth the time invested?

For example – I had to pay my travel agent for flights while we were visiting family in Ireland.

I wanted a fare with a stopover in a new city, and after a quick email exchange, we locked in flights with a bonus detour to Hong Kong.

The catch? A 2% credit card merchant fee.

With seven days to pay, I ran the numbers to see if an international transfer could beat the fee.

Paying by card would’ve cost an extra $130–$155.

By transferring the money into our Irish bank account and paying in euros with a debit card, I could avoid that.

I use a rule of thumb: if saving money takes less time than I’d be willing to work for $20 an hour, it’s worth it.

Setting up with a new currency conversion service (Wise – highly recommend them) took about 30 minutes—ID upload, deposit, done.

The transfer landed in under 24 hours, cost just €3, and saved me over $150. Not bad for half an hour’s effort!

I spent 30 minutes learning how to use the new platform and saved over $150. In this instance, my time was well spent.

But driving across town to a supermarket offering half-price milk is probably not worth my time.

💡 Your time is money too—don’t waste it chasing tiny savings.

Bonus Question: Would Future Me thank me for this purchase or roll her eyes?

If it’s the latter, you probably don’t need it.

The point isn’t to second-guess every single purchase – it’s to make spending a choice instead of a habit.

Ask these 5 questions often enough, and you’ll be surprised how quickly your savings stack up.

Read next: 9 Benefits of Frugality That Are More Important Than Money