It’s been a long while since I’ve written anything personal on this website BUT we hit such a major milestone recently that I just had to share it.

On Friday, 31 December 2021, at 10.22 am my husband handed in his letter of resignation.

We have finally achieved our early semi-retirement goal.

This means we have enough to semi retire right now and will still reach full early retirement within the next ten years.

How we semi-retired early

This plan has been such a long time in the making.

First, we nailed consumer debt, and then we saved enough to travel around the world with our young child, taking off overseas in 2014.

We were gone for 15 months, and it was the impetus for changing our lifestyle and pursuing our version of financial independence.

After we decided we’d really like to travel forever, our goal became creating a location-independent income.

At the same time, we lived as frugally as possible, downsizing to a teeny tiny house that most people probably wouldn’t live in, driving an old Toyota Corolla, which still has many good years in her.

We saved and invested every dollar of my income while paying for our living costs solely on my husband’s wage.

(Here are my original blog posts written in 2015 and 2016 if you’re interested in the beginning of the plan: How I’m Creating a Life I Don’t Need to Retire From and How to Semi-Retire in Your 30s).

Our Actual FIRE Numbers

Yes – I’m sharing our actual numbers. I’ve battled with this, but real numbers were so helpful to me as examples of how other people do things.

I hope I don’t regret this decision.

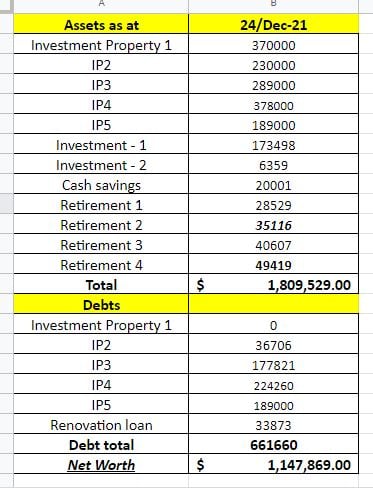

Below is a screenshot of our net worth as of Christmas Eve, 2021.

(The values of all the properties are conservative estimates, considering the insane property boom we’ve just experienced.)

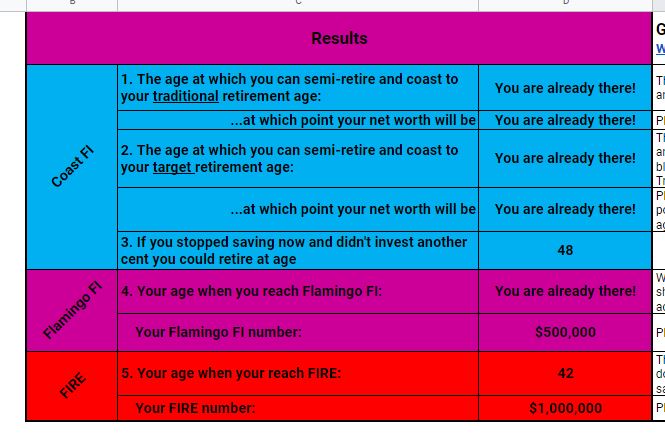

Our FIRE number is 1 million in investments and a paid-off house.

We can and do live an excellent life for $40,000 per year. This is primarily because we do not have a housing cost to contend with.

We live in Investment Property 1 on the above chart.

We still consider it an investment property as it was purchased with the intent of being a rental property – we even had the purchasing documents witnessed by a notary public in Mexico on our travels. He thought we were bonkers.

The property was rented to tenants for many years before we moved into it, and we plan to rent it while we travel, so I include it in our net worth.

As a paid-off property, the rental income it generates will provide an income stream that should cover the rent we have to pay in the places we travel to. The property should rent for around $400/week or $1730/month.

That said, it is not part of our FIRE number.

Our current FIRE balance is $1,147,869 (Net worth) – $370,000 (Property) = $777,869

Including property equity in FIRE numbers?

It’s true you can’t spend your equity unless you borrow against it or sell your property.

We might eventually sell two or three properties and put the proceeds into index funds, pay down all the property debt, and live off the rents.

Is living off rental income viable?

Our four properties currently rent for $1255/week combined.

Add in the property we currently reside in, and the combined weekly rental income comes to $1655/week or $86,060 annually.

Costs, including mortgages, rates, insurance, maintenance and professional property management, run at around $60,000 annually, with the mortgages making up $36,000 of that number.

If we were to pay down all of our properties and rent all five out – we would have an income of $86,060 – $24,000 – $62,060.

This number would be $47,060 if we were to reside in IP1 again (as we wouldn’t be paying for professional property management and tend to do our own maintenance on properties we live in).

This is considerably more than the 4% rule would allow us to draw from a million-dollar portfolio in index funds, BUT it comes with more risk (due to a lack of diversification).

Ideally, we would draw half of our income from free and clear rental properties and half from a portfolio of index funds.

But there is no rush to make this distinction yet, as we aren’t retiring completely.

No doubt, the plan will endure many more iterations before we hit the drawdown period of our lives.

The online business provides a full-time income and will fund our living costs for the next two years.

If we were planning to FIRE tomorrow, we’d sell some properties right now to tip the scales back towards shares.

However, we’ve always bought cash flow-positive properties with at least a 7% gross yield.

This means they pay for themselves, so hanging on to them does not affect our plans.

You can read a case study on one of our purchases here: Case Study: Cashflow Positive Property in Christchurch

We are mindful that we have passed the peak of the cycle here in New Zealand.

The tides are turning, with interest rates and inflation rising rapidly.

As a result, credit is becoming much harder to access, and house prices are starting to slow.

No big deal, though – we don’t need the money right now, so we’ll keep our properties as a hedge against inflation and use the rents to pay down the debts as quickly as possible.

(I also feel a deep sense of responsibility as a property owner to provide affordable rental homes for my tenants. The housing crisis is ugly, and its impact means selling is more than just weighing up tax, profits, and allocations.)

Risks of this plan

Our most significant risks right now are interest rate rises and tax changes.

Tax changes in New Zealand mean that the interest portion of a rental property mortgage will not be deductible in the future (phased in over 4 years).

This is a ridiculous piece of legislation that is entirely out of step with tax law, which requires businesses to pay tax based on profit, not revenue.

For this reason, we plan to pay down our mortgages as fast as possible. This plan will also mitigate the risk of interest rate rises.

Long-term travel plans

Our plan from April of 2022 is to travel with our kids. Primarily in Europe.

We’ll be starting in Ireland and hopefully end up in Spain for an extended period.

We have a rough plan to travel for two years. With the world the way it is right now, we still don’t know what is going to happen, but it’s good to have a tentative plan.

Will you still be investing in Semi-Retirement?

Yes – but not aggressively.

We aim to invest all surplus rental income and around 10% of our “wage” into a 50/50 split between index funds and paying down investment property debt.

If we find that we actually need the money to enjoy our travels, we’ll stop putting money away. No big deal.

That really is it.

It’s incredible how simple managing money becomes when you get clear of consumer debt and have enough assets to generate income for your future retirement.

Then it’s simply about ensuring you have enough to pay your living expenses on a day-to-day basis.

So you’re not actually retiring?

Nope, not me anyway – that’s why it’s called semi-retirement.

My husband has left his physically exhausting job and is now the man of the house doing all the cooking and kid stuff which gives me more time to work on my business.

Which is honestly the best thing ever because I love what I do (plus I hate cooking).

Just knowing that we can live our life on our terms from here on out is incredible.

Being able to earn income wherever we go is what I’ve always dreamed of.

As I wrote on my Spain travel blog:

I like working. I like the structure and having objectives to achieve. Before I had my son I worked up to three jobs at a time. Not just because I like money… There is something to be said for a life combining fulfilling work with the freedom to change your surroundings whenever you choose.

Semi-retirement really is the best of both worlds.

If you’re chasing FIRE, just remember there are no hard rules, and if the RE bit isn’t your cup of tea, you can ignore that part and just enjoy financial independence and the security it brings.

It’s like a big warm money blanket cuddling you to sleep each night.

Resources that deserve a mention – Big thanks Tina from Money Flamingo for her awesome concept and calculator.

It brought home for me that we could indeed frontload our investments and then coast our way to financial independence.

This strategy for turning equity into income from Strong Money Australia has helped me devise a strategy for turning property equity into FIRE planning.

Have you considered semi-retirement as an alternative to early retirement?